Sovereign Solvency

How does America escape its fiscal trap?

Risk & Progress explores risk, human progress, and your potential. My mission is to educate, inspire, and invest in concepts that promote a better future for all. Subscriptions are free. Paid subscribers gain access to the full archive and Pathways of Progress.

This article is part of The Boyd Institute’s quarterly policy sprint on the debt and deficit. To learn more about them and the work they do, or submit your own article, click here.

The United States carries a public debt that now exceeds $39 trillion and counting; a truly enormous burden, even for the world’s largest economy. This challenge is far from unique to America. Many of the world’s most advanced nations now face similar fiscal pressures, with total public debts now matching or surpassing their annual GDPs. Compounding the problem, economic growth in these countries has slowed markedly, sharply reducing the likelihood that they will ever meet their obligations in full. A superficial budgetary review might suggest that runaway entitlement spending or inadequate revenues are the culprit. These conventional diagnoses, however, miss the deeper issue. To confront this crisis meaningfully, we must set aside surface-level explanations and examine the problem from first principles. We must identify the true root cause, the fundamental driver behind these unsustainable trajectories. Only with that clarity can we hope to design an effective corrective mechanism.

Drowning in Debt

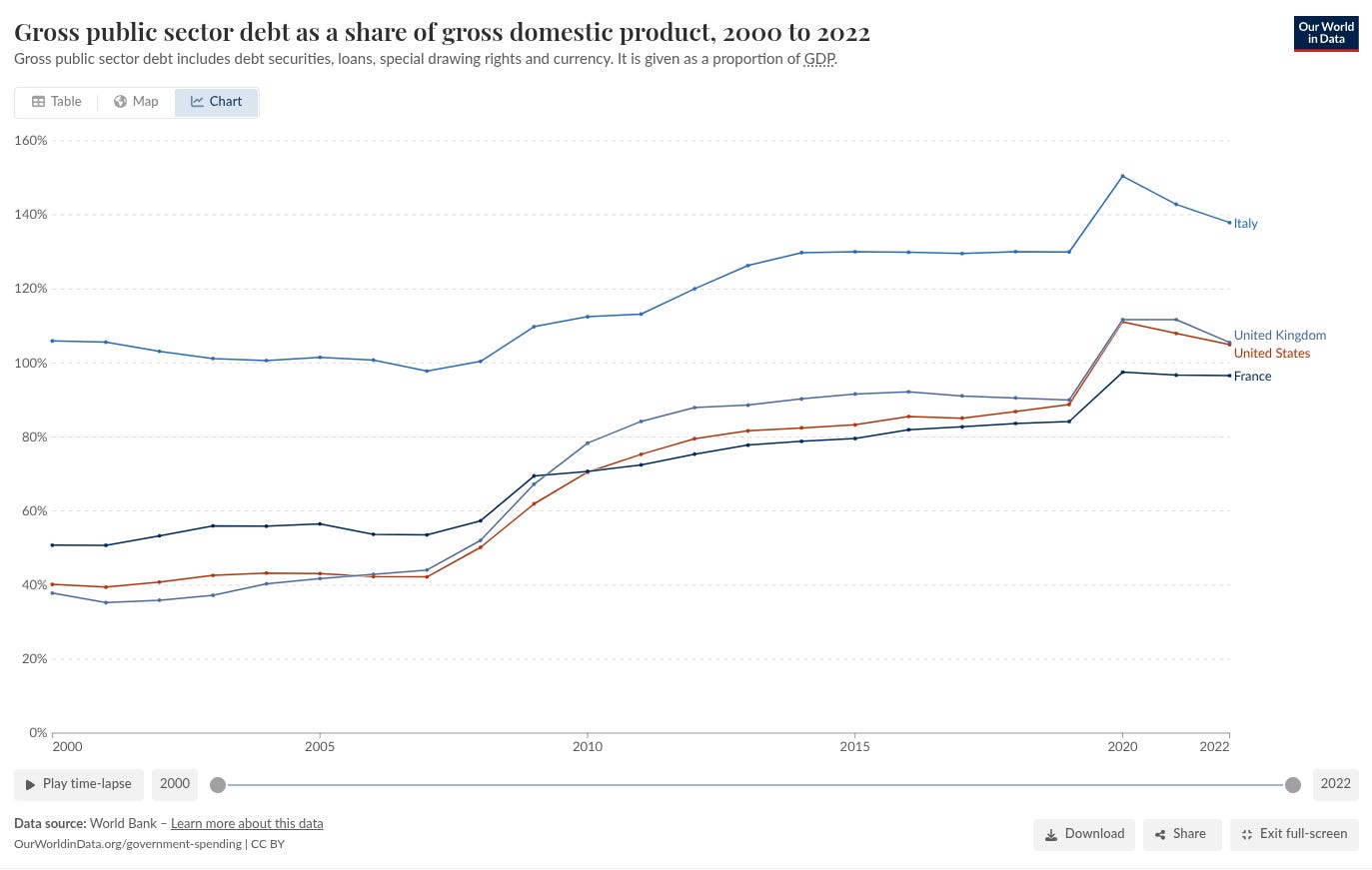

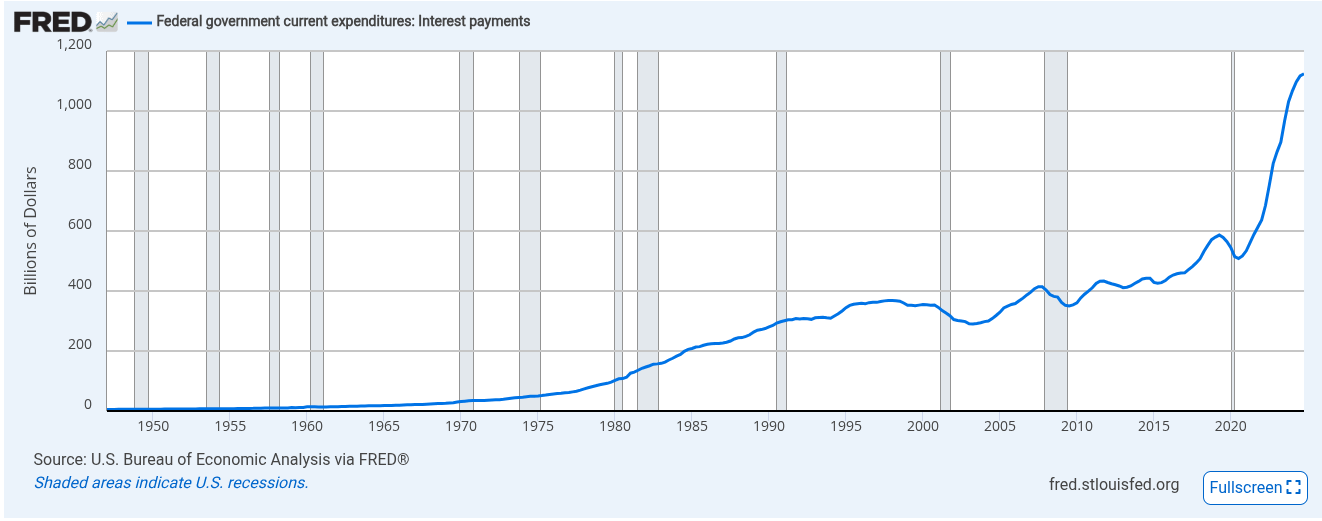

I want to be clear on one issue from the outset: debt is a problem of magnitude. There is no inherent requirement that a sovereign government, one that can print and tax in its own currency, always have a balanced budget. The United States has run a fiscal deficit for most of its existence and zeroed out its Federal debt only once, back in 1835. When productivity is rising, it can be logical to borrow from the future to live better today. Our debt troubles aren’t about the existence thereof, but that it has grown too fast for too long. Many of the world’s most “advanced” nations now carry a debt-to-GDP ratio over 100 percent, levels not seen since the mid-1940s, in the wake of the Great Depression and the Second World War. Then, we had a plausible excuse; today, we have no reason to run these kinds of deficits. Equally worrisome is the cost of maintaining this debt; the United States now spends about 15 percent of its budget just making interest payments. This is flatly unsustainable.

It’s not difficult to understand how we got here. If we think 4th dimensionally, the seats of our Congresses and Parliaments are not only filled by representatives who sit in them today but also by those who will sit in them tomorrow. The problem is that we can only count the votes made by representatives sitting in those seats today. Sure, future representatives and voters are out there, playing tag on a playground somewhere, enjoying a video game, doing homework, lying in a bassinet, etc, but they are, for the moment, voiceless. Consequently, representatives seeking votes today have found that the easiest way to “bring home the bacon” is to make the bill tomorrow’s problem. I’ve discussed this immoral, “government myopia” problem before. This “tyranny of the present” means that immediate concerns, preferences, and desires take precedence over long-term challenges.

In the United States, this has created a vicious dynamic. When the Democratic Party is in power, it passes new spending measures designed to satisfy its voters, but then defers the painful tax hikes needed to pay for them. Likewise, when the GOP returns to power, it cuts taxes and defers the spending cuts. Neither party is willing or able to tackle the core drivers of the Federal deficit, namely Medicare, Social Security, and defense spending, line items which account for more than 80 percent of the projected deficit increase through 2032. Instead, all they can do is rearrange the deck chairs on the Titanic, tinkering around the edges, leaving the deeper problem wholly intact. How can we escape this fiscal trap? In the end, the ledger must balance. This leaves us with four options: print more money, raise taxes, cut spending, or outgrow the debt.

Escaping the Fiscal Trap

Let’s begin with the idea that we can just “print” our way out of a debt crisis. This view is primarily advocated by the “Modern Monetary Theory school” of economists. They contend that public debt is not a problem because a sovereign government can always print more currency to pay it. This is wrong. Governments borrow money by selling bonds. These bonds are like “mini loans” that must be repaid. Sovereign leviathans are not magically immune to their debt obligations; they just default differently. There are two ways to default: a “hard default,” where bondholders take formal written losses, and its worse cousin, a “soft default.” In a soft default, the debt is paid by printing worthless currency, literally inflating the obligation away. The government can escape the first by printing money, but it cannot escape the second. Bondholders won’t be fooled; they will stop lending or demand higher interest rates. Printing is not a long-term solution.

Okay, if we cannot print ourselves out of the debt trap without awaking the bond trolls, perhaps all we need to do is raise taxes to bring in more revenue? We won’t need to borrow from the future if we can meet our obligations today. But does raising taxes actually solve the problem? The answer hinges on whether the deficit is a revenue problem or a spending problem. The balance of evidence suggests it’s the latter, not the former. Recall your middle school physics class, where you learned about the nature of an ideal gas and how gases expand to fill any container you place them into. Government spending is a bit like an ideal gas; the amount spent will always expand to use the revenue available to it, and then some. Think about it, why would a politician who seeks to satisfy as many current voters as possible not spend every dollar they can today?

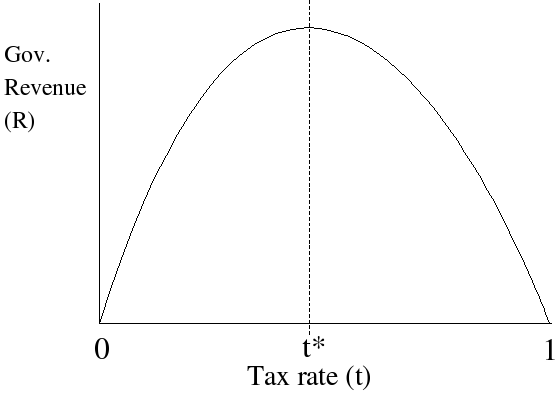

Furthermore, a revenue-side approach to the debt problem is inherently limited, not only because the government will spend every cent it raises, but because continued tax hikes eventually shutter the wealth-creation machine underneath it. Many are probably familiar with the “Laffer Curve,” which suggests there is a maximum amount of tax revenue that the government can raise from a particular tax. The idea is simple: If we tax something at zero percent, we will raise zero dollars in tax revenue. Likewise, if we tax at a rate of 100 percent, we will still raise zero tax dollars. It’s not difficult to understand why; if the government taxed your income at 100 percent, would you still go to work? Therefore, the “optimal” tax rate lies somewhere between zero and one hundred percent, though the rate varies by context and tax type.

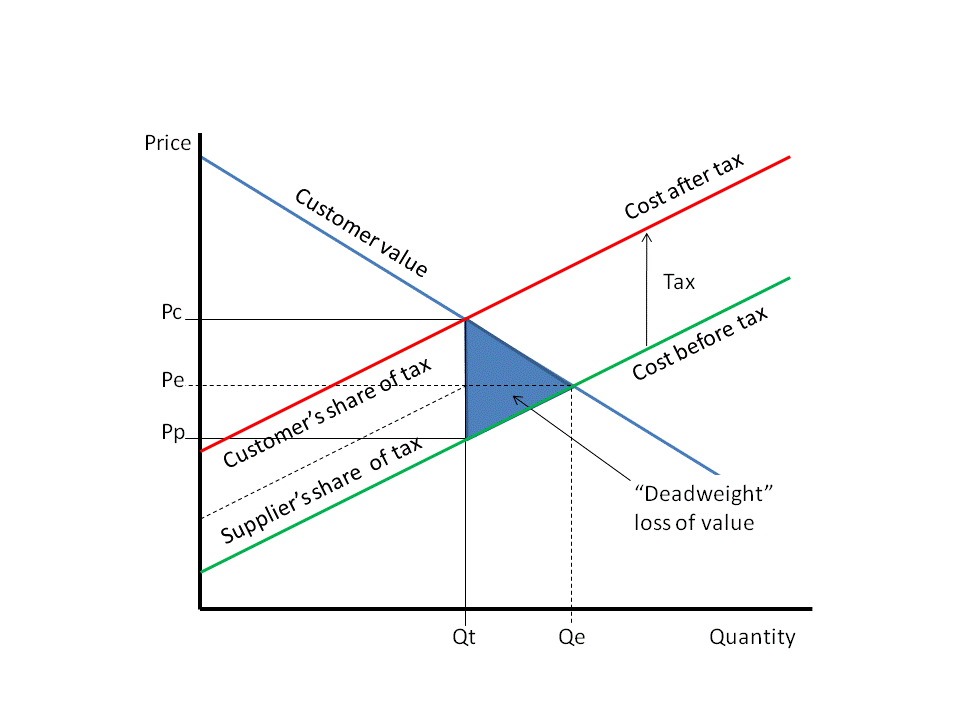

The Laffer Curve is primarily driven by “deadweight loss.” Deadweight loss occurs when the imposition of a tax pushes the normal supply/demand equilibrium out of balance, creating lost economic activity that isn’t translated into revenue. If the government taxes the sale of sofas, for instance, the tax raises the price of buying a sofa. Consequently, some people who may have bought one no longer will, and businesses will sell fewer sofas than they otherwise would have. It’s important to understand, however, that deadweight loss does not scale linearly with the tax rate, but rises to the square of the tax rate. This means that doubling a tax from 10 to 20 percent doesn’t double the economic loss; it quadruples it. So, as we raise taxes, deadweight losses rise faster than revenue, and if we go high enough, the tax base collapses entirely.

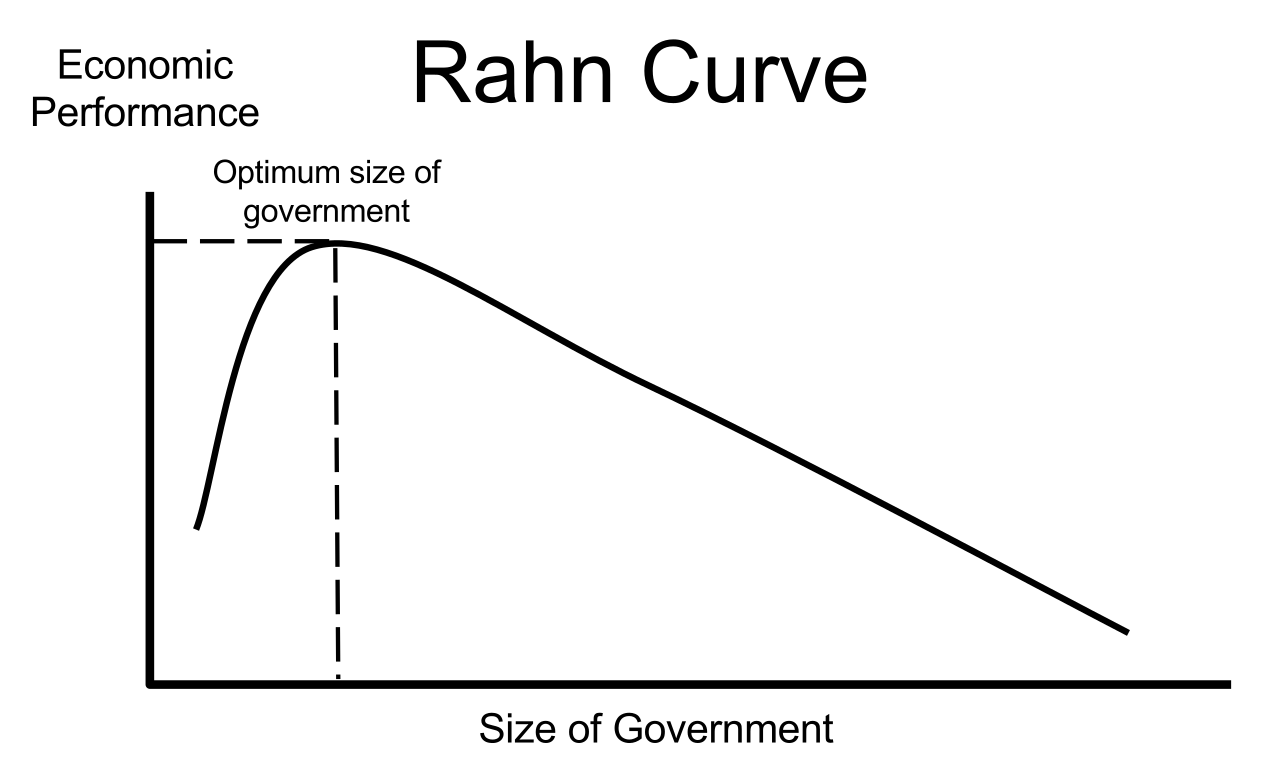

This is why governments that try to tax their way to fiscal solvency never can; the more they raise, the more they inevitably spend, the higher taxes must be, and the more the tax base erodes. In 1996, American economist Richard Rahn analyzed the growth and spending data of all OECD countries, finding that economic growth was strongest when total government spending was ~25 percent of GDP. When government spending exceeds this threshold, growth begins to slow. He caveated his findings with two qualifiers. First, the quality of spending still mattered; we can spend more without imperilling growth if we do so effectively. Second, his findings were probably biased to the high end; the optimal threshold was probably closer to ~15-20 percent of GDP. With many Western governments today spending well over 30-40 percent of their GDP and attempting to tax their way to solvency, we can see why growth is disappointing.

Indeed, large debt loads appear to imperil growth on their own. When government debt is low, spending a little more can accelerate growth, but past a certain threshold, every new dollar of debt has the opposite effect. A seminal 2010 study by Carmen Reinhart and Kenneth Rogoff, for example, found that when public debt exceeds 90% of GDP, the median annual GDP growth falls by about 1 percentage point, and average growth falls even more. Subsequent studies have documented a similar “debt overhang effect,” though the threshold is debated. It’s believed that as debt rises, debt sales soak up capital that would otherwise be directed to more productive uses, stalling growth and forcing ever more distortionary taxes. In sum, while the maximum tax rates, deficit, and debt loads are debated and contextual, we know one thing for certain: high debt, high taxes, and large deficits result in slower growth, which, in turn, makes it even harder to service that debt. The fiscal crisis, therefore, is a spending problem, not a revenue problem.

Cap ‘n Grow

So we have conclusively established that we cannot print or tax our way out of this crisis. This leaves us with two remaining options: either we must cut spending or outgrow the debt. This is, from what we learned above, a bit of a false choice; they are very much the same. If we keep spending and taxes within a reasonable threshold, the economy will grow faster and, over time, make the debt less relevant. Recall that I compared government spending to an ideal gas. I was deliberately echoing Parkinson’s Law, a semi-satirical observation made by British naval historian C. Northcote Parkinson who noted that even as the number of ships and naval personnel in the Royal Navy declined, the number of administrators grew about 6% annually. He reasoned that growth was not driven by increased workload but by a bureaucratic tendency for officials to create more work for each other, “work expands so as to fill the time available for its completion.”

Parkinson’s Law holds broadly. If you allot yourself an entire day to clean your home, it will probably take the whole day. But if you allot yourself just three hours, you will probably get it done in about three hours. Parkinson’s Law is also why many people attest to being more productive near the end of a tight deadline. In fact, we can leverage Parkinson’s Law for our benefit. Effective strategies include time boxing and the Pomodoro method; by constraining the time available for a task, paradoxically, more gets done. The government is a massive time-buying machine, hiring millions of staffers to complete administrative tasks, to review permits, conduct interviews, etc. The more revenue we provide it, the more man-hours it can afford, the more it will find work to do—even if that work is completely and wholly unnecessary.

This further bolsters my belief that the only solution to America’s fiscal trap is a spending cap, a metaphorical container that limits scope creep. And I believe the balance of evidence requires that the cap be around 20 percent of Gross Domestic Product. This isn’t unheard of. For much of America’s history, Federal government spending was only about 5 percent of GDP. With a firm spending cap, taxes can fall, and when they do, growth will accelerate. We will probably still have a fiscal deficit, but that's okay; it will be much smaller by virtue of the fact that growth will be stronger. Some might argue that reducing government revenue would endanger public services; I’d wager that it would not. After a painful transition period, the government would find a way to deliver substantially similar services within the new constraints.

Indeed, within constraints, there is beauty. Staffers will find efficiencies they hadn’t considered before. Policymakers will be forced to focus their attention on the highest return actions, discarding wasteful, low-impact distractions. With some patience and creativity, in fact, I suspect we will find that a constrained government delivers better public services. I’ve outlined some ideas for how this can be achieved at Risk & Progress. Abolishing student loans, for instance, and replacing them with ISAs, would save billions every year while cutting tuition inflation. Likewise, delivering welfare via cash assistance would be cheaper and more effective than the current hodgepodge of in-kind transfers, and relying more on nudges like mandatory Health Savings Accounts would go a long way to ensuring that the safety net remains, sans the public debt.

The only real question becomes: how do we reliably enforce a spending cap? Congress controls the purse, and any law they write can be overwritten. What we need is a “Ulysses pact” or “Ulysses contract.” The term comes from Homer’s Odyssey, in particular, the scene where Ulysses wanted to listen to the Sirens’ bewitching songs as he and his men sailed by their island home. Ulysses knew the Siren songs would render him irrational, so he ordered his men to put wax in their ears and, for the duration of the journey past the island, to literally tie him to the mast and ignore his orders and his pleas. We need a mechanism like this, something that ties our legislators to the mast, lest they be beguiled by the Siren song of spending our children’s money.

A law, therefore, won’t be enough; we need a Constitutional Amendment that would be near impossible to override. Perhaps we could even call it the Ulysses Amendment. The Amendment would cap annual government spending to within a range of 20 and 22 percent of the prior year’s Gross Domestic Product. This range leaves some room for countercyclical action; during recessions or major calamities, for instance, a majority vote of Congress would allow additional spending at the upper end of the cap. The amendment, however, would not allow such a vote to take place in more than one consecutive calendar year, forcing spending to automatically snap back to under 20 percent. Not only would this amendment enforce fiscal discipline, but it would also provide an incentive to adopt pro-growth policies; if you want to spend, you first have to grow. When we tie ourselves to the mast, we can stop ourselves from borrowing on the backs of our children, and within these constraints, we will grow and prosper like never before.

In the meantime, let’s pass an executive order that if Congress increases the net debt in any year that every Congress person has to send an apology letter to every constituent laying out how much per capita the debt they now owe has increased.

The United States of America has fifty members. It should be easy, in fact it has been done by a columnist I used to follow long ago at Forbes, to compare the fiscal and economic performance of those fifty individual states, and to identify principal components contributing to loss or gain. Measuring and analysing their data as a single entity across so diverse a landscape is the EU all over again.

To restore financial health, there is no alternative to turning off the taps.